Global Equity Outlook

Market CommentaryThe Reflationary Case

The markets are telling a reflationary story right now. Economic growth is broadening, inflation is firming, and risk appetite is healthy. In this environment, history suggests favoring the parts of the global equity market that benefit when growth accelerates: emerging markets, value-oriented stocks, and cyclical sectors.

This isn’t a guess about where the market is heading – it’s a response to where it already is. The data supports a pro-cyclical stance across multiple dimensions: manufacturing activity is expanding, corporate earnings are strong and broadening beyond the mega-cap technology stocks that dominated last year, and credit markets remain healthy. Most importantly, markets are rewarding economic sensitivity.

The key question isn’t whether this setup is attractive right now; it is. The question is how long these conditions persist, and what could change them. We’ll walk through both the opportunity and the risks.

What the Market Environment Favors

The current backdrop favors a pro-cyclical orientation. That means tilting toward:

- Value over Growth: Companies trading at attractive valuations relative to their fundamentals tend to outperform when inflation is firming and growth is broadening. The environment now supports value stocks across both US and international markets.

- Cyclicals over Defensives: Sectors like Technology, Consumer Discretionary, and Industrials benefit when economic activity accelerates. Defensive sectors like Utilities, Consumer Staples, and Healthcare typically lag in reflationary periods.

- International Exposure: Both developed international markets and emerging markets deserve meaningful weight. The US dollar is trading below trend, and global growth momentum is positive – both conditions that historically support non-US equities.

- Economically Sensitive Markets: Within emerging markets, regions with strong economic linkages to global growth, such as Asia ex-Japan and Latin America, are particularly well-positioned.

Recent Shift in Market Leadership

Over the past month, market leadership shifted decisively toward risk assets. Defensive positioning that made sense earlier this year is now a drag on performance.

The rotation has been clear: out of minimum-volatility strategies and defensive sectors, into broad market exposure and growth cyclicals. Technology, Consumer Discretionary, and Industrials are leading, while Utilities, Staples, and Healthcare are lagging.

The message is clear: markets are rewarding economic expansion. Positioning should reflect that reality.

Why This Positioning Makes Sense

The Economic Backdrop

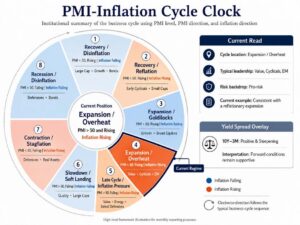

Growth momentum is positive and building. Manufacturing activity (PMI) sits above 50 and is rising, indicating expansion. Inflation is firming alongside economic growth, and the yield curve maintains a positive, steepening slope; all signals that historically support risk-taking in equities.

This is the exact backdrop that favors cyclical positioning. Value stocks, cyclical sectors, emerging markets, and international equities typically need broadening growth momentum and healthy risk appetite to outperform. We have both right now.

Corporate Earnings Are Strong

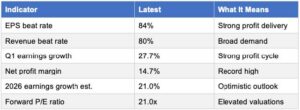

The most recent earnings season delivered impressive results: 84% of S&P 500 companies beat earnings estimates, and 80% exceeded revenue expectations. Year-over-year earnings growth accelerated to 27.7%, while revenue growth came in at 11.3%. Perhaps most importantly, earnings growth is broadening beyond the mega-cap technology names that carried the market through much of last year. Ten of eleven sectors now show year-over-year earnings growth, with seven sectors posting double-digit gains. This breadth of participation supports a cyclical tilt.

That said, concentration hasn’t disappeared completely. A meaningful portion of the upside in aggregate earnings still comes from a handful of large technology and platform companies. The market is broadening, but it’s not yet fully divorced from mega-cap leadership. Continued broadening would strengthen the case for cyclical positioning.

One critical point for a value and cyclical strategy: margins are holding up. The S&P 500 net profit margin hit 14.7% – the highest level on record. Rising inflation is manageable when companies can maintain pricing power and cost control. So far, they can.

Earnings Snapshot

Source: FactSet

Market Conditions Support Risk-Taking

The risk environment has shifted decisively into risk-on mode. Equity volatility is contained, credit spreads are tight, and the US dollar is trading below its trend – all conditions that historically support international and emerging market equities.

The clearest signal comes from market leadership itself: cyclical stocks are outperforming defensive stocks across the US, developed international markets, and emerging markets. When cyclicals lead globally, it tells you that markets are rewarding economic sensitivity. That validates a pro-cyclical stance.

What Could Derail This Setup

This setup is compelling, but it’s not without risk. A pro-cyclical stance concentrated in value stocks, cyclical sectors, and emerging markets creates vulnerability if the conditions supporting these areas reverse.

The primary risk scenario: a resurgence of inflation that drives bond yields sharply higher and strengthens the US dollar. This combination would disproportionately pressure emerging markets, cyclicals, and international equities.

Specific warning signs to monitor:

- US dollar breaking above its 200-day moving average, creating headwinds for international equities

- 10-year Treasury yields rising more than 50 basis points, challenging cyclical stocks and equity valuations

- High-yield credit spreads widening significantly, signaling deteriorating risk appetite

- Global manufacturing activity (PMI) falling back below 50, weakening the growth thesis

- Defensive stocks beginning to outperform cyclicals, signaling a shift in market sentiment

- Emerging markets underperforming developed markets, challenging the case for EM exposure

Any combination of deteriorating growth, tightening liquidity, rising yields, widening credit spreads, or renewed dollar strength would hit cyclical positioning disproportionately hard. These are not distant theoretical risks; they’re the specific conditions that would invalidate the current opportunity. That’s why monitoring them is essential.

The Bottom Line

The market environment favors a reflationary playbook, and right now, that thesis is playing out. Economic growth is broadening, earnings are strong, risk appetite is healthy, and markets are rewarding cyclical exposure.

The setup is constructive for value-oriented stocks, cyclical sectors, and international markets, particularly emerging markets. These areas benefit from the current combination of expanding growth, firming inflation, and accommodative liquidity conditions.

The core issue isn’t whether this asset mix aligns with today’s environment. It clearly does. The real task is keeping a close eye on the macro drivers that justify the stance: tracking growth momentum, inflation trends, credit conditions, currency swings, and shifts in market leadership. If the underlying data changes, our positioning needs to shift with it. For now, the tactical opportunity is compelling, and the right conditions are in place to capture it.

IMPORTANT DISCLAIMERS AND DISCLOSURES:

The information contained in this presentation has been gathered from sources we believe to be reliable, but we do not guarantee the accuracy or completeness of such information, and we assume no liability for damages resulting from or arising out of the use of such information. Past performance is not indicative of future results.

The views expressed in the referenced materials are subject to change based on market and other conditions. This document may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. The information provided herein does not constitute investment advice and is not a solicitation to buy or sell securities.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, investment model, or products, including the investments, investment strategies or investment themes referenced herein, will be profitable, equal any corresponding indicated historical performance level(s), be suitable for a particular portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

Please note that nothing in this content should be construed as an offer to sell or the solicitation of an offer to purchase an interest in any security or separate account. Nothing is intended to be, and you should not consider anything to be direct investment, accounting, tax, or legal advice to any one investor. Consult with an accountant or attorney regarding individual accounting, tax, or legal advice. No advice may be rendered unless a client service agreement is in place.

Procyon Advisors, LLC is a registered investment advisor with the U.S. Securities and Exchange Commission (“SEC”). This report is provided for informational purposes only and for the intended recipient[s] only. This report is derived from numerous sources, which are believed to be reliable, but not audited by Procyon for accuracy. This report may also include opinions and forward-looking statements which may not come to pass. Information is at a point in time and subject to change.

For additional information, please visit our website at www.procyon.net.

Download PDF BACK