Liberation Day to Independence Day: Tariffs, Tensions, and Triumph

Market Commentary

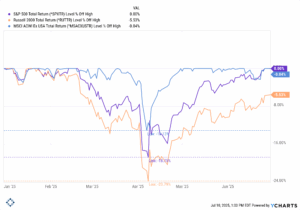

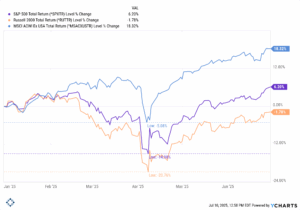

On the surface, the second quarter of 2025 was a blockbuster quarter for equity markets. U.S. and international equities surged over 10%, driven by a powerful rally that took hold in April and rarely let up. Small caps lagged but still posted a solid 8.5% gain.

Taxable fixed income finished slightly positive, while municipals drifted modestly lower.

If you only looked at the numbers, you’d assume investors spent the quarter embracing risk with confidence. But markets rarely move in straight lines—and this quarter’s strength masked a rollercoaster of volatility, uncertainty, and geopolitical shock. While the final story is written above, the chapters that follow offer deeper perspective on what shaped Q2 and where we go from here.

Chapter 1: Tariffs Return with a Vengeance (and So Does Volatility)

The tone for Q2 was set even before it officially began. Markets spent much of Q1 trading lower in anticipation of a shift in U.S. trade policy, and on April 2nd, those fears were realized. In a dramatic speech, former President Trump declared “Liberation Day,” where he announced sweeping tariffs on nearly all imports from countries where the U.S. ran a trade deficit.

Markets responded sharply. U.S. equities plunged, with the S&P 500 dropping nearly 19% from its February peak to the early April trough. The VIX (volatility index) spiked above 50—levels not seen since the pandemic panic of 2020. International markets held up slightly better thanks to a weaker U.S. dollar, but still fell close to 14% from their highs.

The sudden shift in trade policy not only rattled markets—it created deep uncertainty for business leaders and research analysts. With little clarity on the scope or duration of tariffs, many companies began pausing investment plans. We expect these effects to echo through the second half of the year as firms reevaluate capital allocation and supply chain strategies.

Chapter 2: A Pause, Progress, and Promises

Just one week after Liberation Day, the narrative shifted again. On April 9th, President Trump surprised markets by announcing a 90-day pause on the newly announced tariffs. The move was framed as a goodwill gesture to allow space for ongoing trade negotiations, some of which had begun bearing fruit behind the scenes.

The market response was euphoric. The S&P 500 experienced its strongest single-day rally in years, and risk appetite returned with force. From the trough on April 8th to the end of the quarter, major equity indices climbed over 24%.

The 90-day pause was not a resolution, but it was a release valve. It gave markets breathing room and helped anchor the view that extreme trade policy outcomes may be used more for leverage than legislation. While risks remain, investors grew increasingly confident that future tariff headlines would be more bark than bite. That being said, baseline tariffs of 10% remain in place and will have impact on earnings and business investment going forward.

Chapter 3: Powell Holds in the Face of Political Pressure

Coming into the year, markets were pricing in rate cuts by mid-2025. But strong labor market data (unemployment at 4.1%) and inflation that remained above target (Core PCE at 2.7%) kept the Fed firmly on hold.

Chairman Powell and the FOMC opted to stay patient, resisting growing political pressure from President Trump, who has been vocally critical of the Fed’s hesitancy to cut. The Fed’s stance remained cautiously restrictive, aiming to keep inflation on its path toward 2% without jeopardizing the broader economy.

With policy uncertainty (especially on trade and fiscal fronts) still swirling, a wait-and-see attitude is appropriate. The Fed continues to hold a slightly restrictive policy stance, which we believe is appropriate given the economic conditions. Going forward, the Fed finds itself walking a tightrope—balancing economic resilience with political noise, and data dependency with global risk factors.

Chapter 4: Missiles Fly, Markets Hold

Perhaps the most surprising chapter of Q2 came in mid-June, when geopolitical tensions flared dramatically. Israel launched coordinated strikes on Iranian nuclear sites, followed days later by a U.S. air campaign coined Operation Midnight Hammer.

Oil prices surged more than 10% overnight, and headlines warned of a broader regional war. But markets barely blinked. Iran threatened retaliation but ultimately refrained, as President Trump brokered a ceasefire that de-escalated tensions.

By quarter’s end, energy prices had fully retraced their gains, and equities continued their march higher. The market’s muted reaction was a testament to investor focus on fundamentals and a belief that the conflict would remain contained. It was also a reminder of one of our core beliefs: time in the market beats timing the market.

Epilogue: The Story Continues

We’ve already seen significant developments in the early days of Q3. Most notably, the Big Beautiful Bill—a sweeping piece of fiscal legislation—was signed into law on July 4th. The bill includes tax cuts, infrastructure spending, and energy policy changes, and while its full impact will take time to unfold, it’s expected to add meaningfully to the national debt.

The bill comes after Moody’s downgraded the U.S. credit rating in Q2—a sign that debt levels are beginning to catch up with fiscal optimism. As a result, we anticipate higher rates on the long end of the yield curve. The curve remains slightly inverted, but we expect a combination of modest Fed cuts and rising long-term yields to push it toward normalization in the months ahead.

From a macro perspective, we remain constructive. Inflation is moderating, employment remains tight, earnings are resilient, and financial conditions are stable. A more accommodative central bank paired with pro-growth policy may continue to support risk assets. But with rising divergence across market caps, sectors, and styles, selectivity matters more than ever.

Our Positioning

We continue to emphasize broad diversification as essential tools in this market:

- International equities have shown long-awaited leadership after a decade of underperformance.

- Value stocks led early in the year, but growth roared back after April’s lows.

- Small caps still trail, but falling rates and tax relief could act as a catalyst.

- Fixed income has played its role as portfolio ballast during equity drawdowns, particularly in March and early April.

Passive index exposure and concentrated sector/company bets may have worked in recent years—but going forward, we see growing risk in narrow exposures. Discipline, diversification, and a long-term view remain your greatest allies in this fast moving market environment.

Download PDF BACK